Profit when Algorithmic Trading Systems Cause Flashcrashes » książka

Profit when Algorithmic Trading Systems Cause Flashcrashes

ISBN-13: 9781481046787 / Angielski / Miękka / 2012 / 176 str.

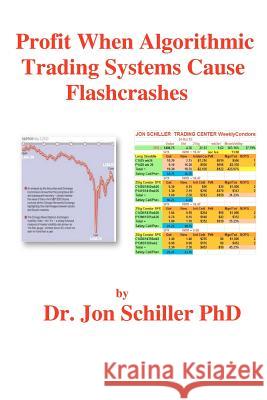

I decided I needed to write this book on Weekly Options trading to see what tactics could be used for the small options trader to combat the volatility caused by Algorithmic trading executed by the big traders such as Banks and Mutual Funds. In 1986 I began Trading Options using Naked Index Spreads with a simple algorithm: Sell Call Options 2 standard deviations (2Sig) above the market and sell Put Options 2Sig below the market. The Initial Credit received for these naked spreads was placed in my broker's trading account. If the market remained less than the Call strike price and greater than the Put strike price at Options Expiration on the third Friday of each month, then the Initial Credit became my profit for the Month for Monthly Options. I now prefer to have less capital at risk so I use covered options trades. When Weekly options became available, I switched to using 2sigma Condors: I sell call options 2 sig above the market and buy call options one strike price higher and simultaneously I sell put options 2 sig below the market and buy put options one strike price lower. The 2 sigma distance above and below the market had a 90% probability of staying safe. In other words you had a 90% probability that your Initial Credit would become your profit at expiration. This is if trading were a random process. For many years this simple 2Sig algorithm worked and your capital grew steadily. However the introduction of sophisticated computer actuated Algorithmic Trading Systems caused distortion of the Global stock, futures and currency markets. Now we saw huge market movements. Sometimes when some financial news was flashed, the market jumped or dropped by more than 2 sigma in one day. Reference: http: //en.wikipedia.org/wiki/2010_Flash_Crash The May 6, 2010 Flash Crash, also known as The Crash of 2:45, the 2010 Flash Crash, or just simply, the Flash Crash, was a United States stock market crash on Thursday May 6, 2010 in which the Dow Jones Industrial Average plunged about 1000 points (about 9%) only to recover those losses within minutes. It was the second largest point swing, 1,010.14 points, and the biggest one-day point decline, 998.5 points, on an intraday basis in Dow Jones Industrial Average history. Wall Street banks and brokers are pouring over their trading systems and rethinking the way they test software to make sure they don't become the next Knight Capital Group, the trading firm whose survival was imperiled by a software glitch on Thursday, 1 August 2012.

Zawartość książki może nie spełniać oczekiwań – reklamacje nie obejmują treści, która mogła nie być redakcyjnie ani merytorycznie opracowana.

Czytaj nas na:

KrainaKsiazek.PL - Księgarnia Internetowa